No. 566: September Employment/Unemployment, August Construction Spending,

COMMENTARY NUMBER 566

September Employment/Unemployment, August Construction Spending,

September Existing Home Sales

October 22, 2013

__________

Weakening Trends Seen in Payrolls and Home Sales

October Payroll Loss of Roughly 400,000 Remains Likely

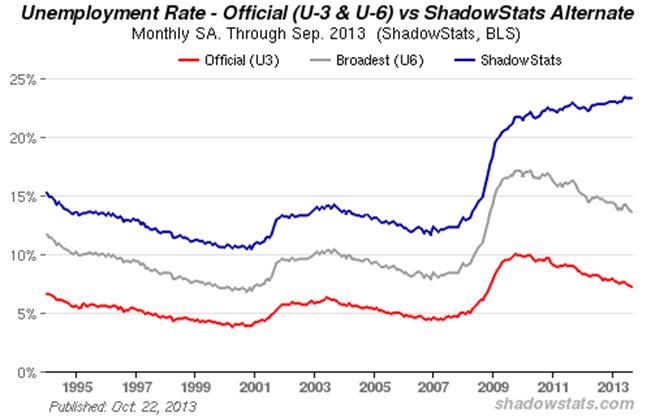

September Unemployment: 7.2% (U.3), 13.6% (U.6), 23.3% (ShadowStats)

Rising Costs Boosted Construction Spending

__________

PLEASE NOTE: The next regular Commentary is scheduled for Friday, October 25th, covering the August trade deficit and September new orders for durable goods. Further Commentaries will follow on Monday, October 28th, covering September industrial production; on October 29th covering retail sales and PPI; and on October 30th, covering CPI, real retail sales and earnings. For available specifics on rescheduled economic series, see the schedule link here, and on the home page at www.ShadowStats.com.

Due to today’s heavier-than-anticipated flow of rescheduled data, and some complications in handling same, the updated Hyperinflation Outlook summary, and detail on the upcoming full revision of the Hyperinflation Report, planned for today, have been pushed to Friday’s (October 25th) Commentary No. 567. The current summary is as published in Commentary No. 564.

Best wishes to all — John Williams

OPENING COMMENTS AND EXECUTIVE SUMMARY

The U.S. Economy Continues to Weaken. The first major economic reporting since the reopening of the federal government has confirmed a deteriorating outlook for U.S. business activity. As shown in the accompanying graph of private payrolls, the pre-government-shutdown employment trends through September were downright negative. On a three-month, moving-average basis, payrolls have been slowing since the beginning of 2013, through September. Private payrolls are shown here, in that they were not distorted by 2010 Census hiring and firing. Although these payrolls will not be hit directly by the October government furloughs, they certainly will reflect secondary impact.

This chart is courtesy of Explistats, a new ShadowStats-related service. In an early stage of development, this site provides access to the details within a growing number of official, economic data releases. A further graphic of total payrolls (including government payrolls), and a link to this work-in-progress site, are provided to our subscribers, in the Employment section of the Reporting Detail.

The story with August construction spending was one of continued stagnation, particularly when considered net of rising building costs. The trends for existing home sales turned negative in September, both in terms of monthly and annual growth, and in terms of indicators of homebuyer or homeowner liquidity.

With the delayed October releases of September and August data rescheduled, only the housing starts and new sales are suffering extensive further delay, into late November and early December.

September Employment and Unemployment. As shown in the preceding graph, payroll employment is trending lower. That is bad news for the economy, and although annual payroll growth is holding in positive territory, it is at levels consistent in normal economic times with looming recession. Headline unemployment also is trending lower, but that also is not an economic positive, where declining unemployment primarily continues to reflect the longer-term unemployed giving up looking for work.

The looming employment and unemployment reporting for October, now due for release on November 8th, will reflect the impact of the government furloughs. As discussed in Commentary No. 564, that should add roughly three-tenths of a percentage point to the headline (U.3) unemployment rate, and push the monthly payroll change down to roughly a 400,000 jobs loss. Much, but not all of that should reverse in the next month’s reporting.

September 2013 Headline (U.3) Unemployment. Headline unemployment fell to 7.2% in September 2013, from 7.3% in August, per the Bureau of Labor Statistics (BLS). The September reading was down from 7.8% from the year before, but that annual decline generally is not good news, as discussed in Commentary No. 521 and Commentary No. 554. Instead of reflecting those who are unemployed finding jobs, the lower headline U.3 rate of recent months generally has reflected those who are unemployed being defined out of the government’s unemployment measurement by restrictive definitions.

Further, the reported September 2013 seasonally-adjusted headline (U.3) unemployment rate of 7.24% simply was not comparable to the 7.28% unemployment rate in August. Again, as with the other headline household-survey data, the problem with unemployment-rate comparability is tied to the use of concurrent-seasonal-factor adjustments.

When the seasonally-adjusted September 2013 unemployment data were calculated, consistent, new seasonal factors also were recalculated for August 2013 and prior months. Based on the new seasonal factors, there is a revised August unemployment rate that is consistent with September’s new headline reporting, but it is not available to the public. Although the BLS knows that number, it will not publish it; it has left intact the now-inconsistent and obsolete number that previously had been reported for August. This issue is discussed further in the Concurrent Seasonal Factor Distortions section.

As a result, the purported headline, 0.1% (0.04% to the second decimal place) month-to-month decline in the September U.3 employment rate could have been an increase, unchanged, or a decline, but no one other than the BLS knows for sure. Even so, the monthly decline in the official U.3 rate was statistically insignificant, based on official error estimates.

U.6 Unemployment Rate. The broadest unemployment rate published by the BLS, U.6 includes accounting for those marginally attached to the labor force (including short-term discouraged workers) and those who are employed part-time for economic reasons (i.e., they cannot find a full-time job).

With minimal monthly changes in people working part-time for economic reasons and short-term discouraged workers, the headline September 2013 U.6-unemployment rate eased back to 13.6%, from 13.7% in August, in tandem with the U.6 decline. Again, though, the monthly seasonally-adjusted numbers are not comparable, and the BLS guesstimates are unstable. The unadjusted September U.6 rate declined to 13.0% from 13.6% in August. In a broader parallel with U.3, the longer-range decline in U.6 partially reflects long-term discouraged workers leaving the U.6 labor force and entering the realm of the ShadowStats alternate measure.

The current official discouraged-worker number reflected the flow of the unemployed—increasingly giving up looking for work—leaving the headline U.3 unemployment category and being rolled into the U.6 measure as short-term “discouraged workers,” net of those moving from short-term discouraged-worker status into the netherworld of long-term discouraged-worker status. It is the long-term discouraged-worker category that defines the ShadowStats-Alternate Unemployment Measure. There appears to be a relatively heavy, continuing rollover from the short-term to the long-term category.

ShadowStats-Alternate Unemployment Rate. Adding back into the total unemployed and labor force the ShadowStats estimate of the growing ranks of excluded, long-term discouraged workers, broad unemployment—more in line with common experience, as estimated by the ShadowStats-Alternate Unemployment Measure—held again at 23.3% in September, as in August and July. July had notched lower from a series high of 23.4% (back to 1994) in June 2013. The ShadowStats estimate reflects the increasing toll of unemployed leaving the headline labor force. Where the ShadowStats alternate estimate generally is built on top of the official U.6 reporting, it tends to follow its relative monthly movements. Accordingly, the alternate measure often will suffer some of the same seasonal-adjustment woes that afflict the base series, including underlying annual revisions.

As seen in the accompanying graph of the various unemployment measures, there continues to be a noticeable divergence in the ShadowStats series versus U.6. The reason for this is that U.6, again, only includes discouraged workers who have been discouraged for less than a year. As the discouraged-worker status ages, those that go beyond one year fall off the government counting, even as new workers enter “discouraged” status, but they remain in the ShadowStats count. See the Household Survey section for further discussion and definition.

September 2013 Payroll Employment. In the context of a small upside (9,000 jobs) revision to the level of August’s payroll employment, a small downside (15,000 jobs) revision to the level of July’s payroll employment, and continued heavily distorted seasonal factors, the September 2013 headline payroll employment gain was a below-consensus 148,000. The August 2013 headline monthly jobs increase was revised to a seasonally-adjusted 193,000 (previously 169,000) gain, versus a revised July gain of 89,000 (previously 104,000, initially 162,000).

An ongoing reporting issue here remains that the BLS publishes only two prior months of consistent data with concurrent-seasonally-adjusted payrolls. Accordingly, where the published July number no longer is consistent with June reporting, related month-to-month comparisons have no meaning, given the BLS adjustment and reporting policies discussed in Concurrent Seasonal Factors Distortions in this Reporting Detail section. On a consistent basis, the July gain versus June was 96,000, not 89,000.

The preceding two graphs are updated for the headline payroll levels through September 2013. The year-to-year rates of change are graphed in the Reporting Detail section. Even with the annual growth seen in the payroll series since mid-2010, the August 2013 level of employment is shy by 1.8-million jobs, or 1.3% in official reporting, from recovering its pre-recession high of January 2008. In perspective, the longer-term plot of employment levels shows the extreme duration of the non-recovery in employment, the worst such circumstance of the post-Great Depression era.

In terms of year-to-year change, the not-seasonally-adjusted annual change is untouched by the concurrent seasonal adjustments, so the monthly comparisons of year-to-year change at least are reported on a consistent basis. For September 2013, the year-to-year percent gain in payrolls slowed to 1.66%, from a revised 1.67% (previously 1.65%) in August, and versus an unrevised 1.66% (initially 1.72%) in July. These levels are consistent with pre-recession periods seen under normal economic circumstances.

Rising Construction Costs Boosted August Construction Spending. Half the August construction spending gain reflected higher building costs, as opposed to increased volume in physical activity. Accordingly, total construction spending continued a monthly pattern of low-level stagnation.

Although the general trend—even in nominal terms—has been minimally to the upside since 2011, monthly changes rarely have been statistically significant. The general pattern of activity has been one of plunge (starting in 2006) and stagnation (starting in 2011), not the hyped-GDP pattern of plunge (starting at the end of 2007) and ever-after recovery (starting in mid-2009). Those construction trends can be seen in the accompanying inflation-adjusted graph. More-comprehensive graphs, in the Reporting Detail section, show detail by type of construction since 2000.

The total, nominal value of construction put in place in the United States during August 2013 was $915.1 billion, on a seasonally-adjusted annual-rate basis. That estimate was up month-to-month by a statistically-insignificant 0.6% +/- 2.5% (all confidence intervals are at a 95% level), versus a revised $909.4 (previously $900.8) billion in July. Before prior-period revisions, July reporting would have reflected a monthly gain of 1.6%. Adjusted for PPI new construction inflation, aggregate real spending in August 2013 was up by 0.3% month-to-month, versus a 1.4% gain in July.

On an annual-growth basis, August 2013 construction spending was up year-to-year by a statistically-significant 7.1% +/- 2.7%, versus a revised July annual gain of 6.2%. Net of construction costs indicated by the PPI current construction index, year-to-year growth in spending was 5.7% in August, 4.1% in July 2013.

The statistically-insignificant 0.6% gain in monthly August 2013 construction spending included a 0.4% monthly gain in public construction spending, versus a revised 0.1% month-to-month gain (previously a 0.3% contraction) in July. August private construction was up by 0.7%, following a revised 1.9% (previously 0.9%) gain in July.

September Existing Home Sales Trends Showed Deterioration. Signaling renewed difficulties in the sales of existing home, September sales saw a dip in monthly activity, a deteriorating pattern of annual sales growth, rising distressed sales for the month, and increasing all-cash sales (along with likely related deterioration in banking-system liquidity) on both a month and annual basis.

September monthly home sales fell by a headline 1.9% month-to-month (counted based on actual closings, National Association of Realtors [NAR]). The monthly decline would have been 3.5% without the downside revision to August sales. Annual growth continued to slow, and the latest activity remained 27.2% below the June 2005 pre-recession high for the series. Year-to-year growth continued to slow, dropping to 10.7% in September, from 11.4% (previously 13.2%) in August, from its near-term peak of 17.2% in July.

Given questions of the series’ reliability, particularly the quality of, and the volatility, instabilities and uncertainties in the reporting of existing-home sales, not too much should be read into the reported trends. These data will be reviewed in the context of new home sales and residential construction, at such time as those series are published.

Smoothed for irregular distortions, the series remained statistically consistent with a period of broad stagnation that has turned into a faltering uptrend, as suggested by the accompanying graph. Nonetheless, as discussed most recently in Commentary No. 564, there have been no developments in underlying economic fundamentals that would suggest a pending housing-industry turnaround or broad economic recovery.

Consumer and Banking-Industry Liquidity Problems. The portion of total sales in distressed properties rose in the latest reporting, from August’s post-2008 Crisis low. The NAR estimated “distressed” sales in September 2013 jumped to 14% of the total (9% foreclosures, 5% short sales), versus 12% of the total (8% foreclosures, 4% short sales) in August.

Reflecting ongoing lending problems, related banking-industry and consumer solvency issues, and the continuing influx of speculative investment money into the existing housing market, the NAR also estimated that all-cash sales in September 2013 were at 33% of the total, up from 32% in August 2013 and 28% in September 2012.

[For further detail on the September employment and unemployment,

existing home sales, and August construction spending, see the Reporting Detail section.]

__________

HYPERINFLATION WATCH

Hyperinflation Outlook—Summary. Due to the unexpectedly heavy flow of new data this morning and some complications in getting and processing same, the updated summary for the Hyperinflation Outlook, planned for today, has been pushed to Friday’s (October 25th) Commentary No. 567. The current summary remains as published in Commentary No. 564.

__________

REPORTING DETAIL

EMPLOYMENT AND UNEMPLOYMENT (September 2013)

Payroll Trend Was Slowing Even Before the Government Shutdown. The following graph shows the three-month, moving-average of monthly changes in total nonfarm payrolls, including government employment. Private payrolls are graphed in the Opening Comments section and are courtesy of our affiliate Explistats.

EXPLISTATS. For more details of today’s employment reports you may find of interest ExpliStats.com, a new ShadowStats-related service. At this point, only ShadowStats subscribers have been made aware of our affiliate. In an early stage of development, this new site provides access to the details within a growing number of official, economic data releases. For example, on this page: http://explistats.com/economic-activities/payroll-survey-latest-data-charts/ you will find various charts and tables bringing out some interesting features in today’s payroll survey. The graphs shown here and in the Opening Comments section were customized by Explistats for ShadowStats.

The current downtrend here is before a pending downside benchmark revision to the current payroll series. The “upside” part of the pending “upside” benchmark revision announced on September 26th, involved adding in a new employment group, which also should be added into a restated history of the series, with little near-term impact on relative activity. The regular benchmarking was to the downside.

That data in the graph include government payrolls, reflecting the impact of 2010 Census hiring and firing. The chart next month will show the impact of the October 2013 government furloughs. Again, economic activity was deteriorating here before the federal government shutdown.

September Labor Data Suggested a Deteriorating Economy. The broad economic outlook has not changed, although the economic downside still should be picking up a little momentum among consensus forecasters. Indeed, payroll employment is trending lower. That is bad news for the economy, and although annual payroll growth is holding in positive territory, it is at levels consistent in normal economic times with looming recession. Headline unemployment also is trending lower, but that also is bad news for the economy, where the declining headline unemployment rate continues primarily to reflect the longer-term unemployed giving up looking for work.

PAYROLL SURVEY DETAIL. In the context of a small upside (9,000 jobs) revision to the level of August’s payroll employment, a small downside (15,000 jobs) revision to the level of July’s payroll employment, and continued heavily distorted seasonal factors, the BLS reported this morning, October 22nd, a seasonally-adjusted, month-to-month headline payroll employment gain of 148,000 for September 2013. Net of prior-period revisions, the monthly gain would have been 157,000. Where the standard 95% confidence interval on the headline monthly change in payroll employment reporting is +/- 129,000, circumstances suggest that a much wider confidence interval could be justified. The current numbers continue to be so far out of balance as to be absolutely meaningless, here, due partially to concurrent-seasonal-factor distortions (discussed in the Concurrent Seasonal Factor Distortions section).

The August 2013 headline monthly jobs increase was revised to a seasonally-adjusted 193,000 (previously 169,000) gain, versus a revised July gain of 89,000 (previously 104,000, initially 162,000).

The ongoing reporting issue here remains that the BLS publishes only two prior months of consistent data with concurrent-seasonally-adjusted payrolls. Accordingly, where the published July number no longer is consistent with June reporting, related month-to-month comparisons have no meaning, given the BLS adjustment and reporting policies discussed in Concurrent Seasonal Factors Distortions in this Reporting Detail section.

Using the latest concurrent seasonal-factor calculations from the BLS, ShadowStats is able to estimate that the consistent, actual revised (but not published) month-to-month gain for July versus June was 96,000, instead of the official 89,000. The month-to-month reporting discrepancies go in both directions and usually are greater than the July difference of 7,000, with monthly differential magnitudes approaching 100,000 jobs, on occasion.

The BLS explains that it avoids publishing consistent, prior-period revisions so as not to “confuse” its data users. No one seems to mind if the published earlier numbers are wrong, particularly if unstable seasonal-adjustment patterns have shifted prior jobs growth into current reporting, without any indication of same in the published historical data.

2013 Benchmark Revision. As discussed in Commentary No. 526, of September 26th, the announced benchmark revision to the 2013 payroll survey would be tantamount to fraud, if the entire historical series is not otherwise revamped for a major redefinition of nonfarm payrolls. As standardly reported, the March 2013 benchmarking lowered the payroll levels of that time by 124,000 jobs, instead of the 345,000 “increase” reported, which included 469,000 new workers who were classified and defined previously as not counted in nonfarm payrolls.

Indeed, as it has been configured, the payroll employment level in the benchmark month of March 2013 was found to have been overstated by 124,000 jobs, requiring a downside revision to the series in that month, with adjustments back to March 2012, and with adjustments forward in time through the reporting of January 2014 payrolls (to be released in February 2014). In the later months of the revision cycle, the downside revisions to monthly levels likely would have topped 200,000.

In a turnaround, the announced benchmark revision was restated so as to be to the upside by 345,000, thanks to the inclusion of 469,000 in employment that previously had not been counted as part of the nonfarm payroll survey. Aside from excluding agricultural employment, the payroll survey had excluded those on household payrolls. Now 469,000 of the household payrolls have been moved into the payroll survey, into the education and healthcare industries, and there is no indication that the BLS plans to restate prior history so as to have a consistent historical series.

Further, this is an area that is not surveyed easily by the BLS on a monthly basis, so it becomes a new fudge-factor for re-jiggering the headline payroll numbers. As announced by the BLS:

“Each year, [payroll] employment estimates from the Current Employment Statistics (CES) survey are benchmarked to comprehensive counts of employment for the month of March. These counts are derived from State Unemployment Insurance (UI) tax records that nearly all employers are required to file. For National CES employment series, the annual benchmark revisions over the last 10 years have averaged plus or minus three-tenths of one percent of Total nonfarm employment. The preliminary estimate of the benchmark revision indicates an upward adjustment to March 2013 Total nonfarm employment of 345,000 (0.3 percent). This revision is impacted by a large non-economic code change [made by the BLS] in the Quarterly Census of Employment and Wages (QCEW) that moves approximately 469,000 in employment from Private households, which is out-of-scope for CES, to the Education and health care services industry, which is in scope. After accounting for this movement, the estimate of the revision to the over-the-year change in CES from March 2012 to March 2013 is a downward revision of 124,000.”

Trend Model. As described generally in Payroll Trends, the trend indication from the BLS’s concurrent seasonal-adjustment model is for a 67,000 monthly payroll gain in October 2013, based on September’s reporting. This excludes any anticipated impact from the recent shutdown in some federal government activity.

The trend indication often misses actual reporting. The indication for September was for a 181,000 monthly gain, which effectively became the market expectation, but it was higher than the actual headline gain of 148,000. Where the trend number usually becomes the basis for the consensus outlook, the consensus forecast will adjust that number for expected shutdown impact.

Annual Change in Payrolls. Not-seasonally-adjusted, year-to-year change is untouched by the concurrent seasonal adjustments, so the monthly comparisons of year-to-year change are reported on a consistent basis. For September 2013, the year-to-year percent gain in payrolls slowed to 1.66%, from a revised 1.67% (previously 1.65%) in August, and an unrevised 1.66% (initially 1.72%) in July.

The preceding graphs of year-to-year unadjusted payroll change reflect near-term detail as well as seventy-plus years of history. Graphs of seasonally-adjusted payroll levels are found in the Opening Comments. Year-to-year change had shown a slowly rising trend in annual growth into 2011, which reflected protracted bottom-bouncing in the level of nonfarm payrolls. That pattern of annual growth flattened out in late-2011 and began a pattern of slowing-to-flat growth early in 2012.

With the bottom-bouncing patterns of recent years, current annual growth has recovered from the post-World War II record 5.06% decline seen in August 2009. That 5.06% decline remains the most severe annual contraction since the production shutdown at the end of World War II (a trough of a 7.59% annual contraction in September 1945). Disallowing the post-war shutdown as a normal business cycle, the August 2009 annual decline was the worst since the Great Depression.

Still, even with the annual growth in the series since mid-2010, the September 2013 level of employment is shy by 1.8-million jobs, or 1.3% in official reporting, from recovering its pre-recession high. In perspective, the longer-term graph of the employment level (see Opening Comments), shows the extreme duration of the non-recovery in payrolls, the worst such circumstance of the post-Great Depression era.

Concurrent Seasonal Factor Distortions. As reflected in the accompanying graph, seasonal-factor instabilities continued in the latest payroll reporting. Still, the BLS never brings the bulk of related reporting issues before the public.

There are serious and deliberate reporting flaws with the government’s seasonally-adjusted, monthly reporting of employment and unemployment. Each month, the BLS uses a concurrent-seasonal-adjustment process to adjust both the payroll and unemployment data for the latest seasonal patterns. As each series is calculated, the adjustment process also revises the history of each series, recasting prior reporting on a basis that is consistent with the new seasonal patterns of the headline numbers.

The BLS, however, uses the current estimate but does not publish the revised history, even though it calculates the consistent new data each month. As a result, headline reporting generally is neither consistent with nor comparable to earlier reporting, and month-to-month comparisons of these popular numbers usually are of no substance, other than for market hyping or political propaganda.

September Inconsistencies. For September 2013, the headline unemployment rate was 7.2%, and the headline monthly payroll gain was 148,000 jobs. Yet, the September unemployment rate was neither consistent with nor comparable to the August unemployment rate of 7.3%. While the 148,000 jobs gain for September was consistent with the revised 193,000 jobs increase in August, on a concurrent-seasonally-adjusted basis, those increases were not consistent with the revised 89,000 jobs gain reported for July or with any earlier published data. The August number would have been consistent with a 96,000 jobs gain in June.

Unemployment Numbers Simply Are Not Comparable Month-to-Month. Except for the once-per-year December release of revisions to seasonally-adjusted data, the BLS publishes no revised seasonally-adjusted data on a monthly basis for the household survey, even though those revisions are made and are available internally to the BLS for publication every month, as part of the concurrent-seasonal-factor process. Accordingly, the reported 0.1% decline in September U.3 unemployment, at 7.2%, versus 7.3% in August, was of no meaning. The unemployment rate could have been up, down or unchanged; there just is no way to know from existing BLS reporting.

As discussed frequently (see Commentary No. 473, Commentary No. 461, and Commentary No. 451, for example), the revisions to earlier data from the concurrent-seasonal-factor process can be significant. As a result, month-to-month changes in seasonally-adjusted unemployment rates are meaningless—not determinable under current BLS reporting policies—and use of monthly comparisons simply should be avoided. At this time, the BLS does not make usable, comparative data available to the public.

Payroll Growth Is Consistent Only One-Month Back, With Heavy Distortions Usual. With the payroll series, the level of payrolls is released for the headline month, and for the two prior months, on a consistent basis. That means that only the current headline month-to-month change and the change for the prior month are consistent and comparable. Unlike the household-survey circumstance, however, the BLS makes available the seasonal-adjustment models and data so that others can calculate the payroll revisions, and ShadowStats has done so for the accompanying graph. All these data were reset with the March 2012 benchmark revision, which was published in January 2013.

Distortions in the post-benchmark environment are evident, even though the first data were based on the initial public reporting of the benchmark revision. The reason for this is that the benchmark revision actually was run internally by the BLS, based on October 2012 numbers. With subsequent internal runs in November, December and January 2013, three months of revisions already had skewed the January data, as shown in the accompanying graph. The line for February reflects only one month subsequent of new seasonal-factor revisions, the March line reflects a second month and so on through June, with mounting seasonal instabilities. Without distortions, the plotted lines would be flat and at zero.

Conceivably, the shifting and unstable seasonal adjustments could move 90,000 jobs or more, in either direction (based on last year’s full revisions, and approached by this year’s numbers) in earlier periods and insert them into the current period as new jobs, without there being any published evidence of that happening.

Note: The issues with the BLS’s concurrent-seasonal-factor adjustments and related inconsistencies in the monthly reporting of the historical time series are discussed and detailed further in the ShadowStats.com posting on May 2, 2012 of Unpublished Payroll Data.

As discussed in other writings (see for example Hyperinflation 2012), seasonal-factor estimation for most economic series has been distorted severely by the extreme depth and duration of the economic contraction. These distortions are exacerbated for payroll employment data based on the BLS’s monthly seasonal-factor re-estimations and lack of full reporting.

A further issue remains that the month-to-month seasonally-adjusted payroll data have become increasingly meaningless, with reporting errors likely now well beyond the official 95% confidence interval of +/- 129,000 jobs in the reported monthly payroll change. Yet, the media and the markets tout the data as meaningful, usually without question or qualification.

Birth-Death/Bias-Factor Adjustment. Despite the ongoing, general overstatement of monthly payroll employment, the BLS generally adds in upside monthly biases to the payroll employment numbers. The regular overstatement is evidenced usually by regular and massive, annual downward benchmark revisions (2011 and 2012, excepted). As discussed in the Benchmark Revision section above, the just announced standard benchmarking confirmed an overstatement of payroll levels and growth as of March 2013. Without new gimmicks added to the process (again, see the Benchmark Revision section), current reporting would be running at a payroll level roughly 200,000 jobs lower, based on that benchmark

The upside-bias process was created simply by adding in a monthly “bias factor,” so as to prevent the otherwise potential political embarrassment of the BLS understating monthly jobs growth. The “bias factor” process resulted from such an actual embarrassment, with the underestimation of jobs growth coming out of the 1983 recession. That process eventually was recast as the now infamous Birth-Death Model (BDM), which purportedly models the effects of new business creation versus existing business bankruptcies.

September 2013 Bias. The not-seasonally-adjusted September 2013 bias was a monthly add-factor of minus 26,000, versus minus 14,000 in September 2012 and a positive 90,000 add-factor in August 2013. The aggregate upside bias for the trailing twelve months notched declined to 609,000 in September, from 621,000 in August, or to a monthly average of roughly 51,000 jobs created out of thin air, on top of some indeterminable amount of other jobs that are lost in the economy from business closings. Those losses simply are assumed away by the BLS as part of the BDM, as discussed below.

Problems with the Model. The aggregated upside annual reporting bias in the BDM reflects an ongoing assumption of a net positive jobs creation by new companies versus those going out business. Such becomes a self-fulfilling system, as the upside biases boost reporting for financial-market and political needs, with relatively good headline data, while often also setting up downside benchmark revisions for the next year, which traditionally are ignored by the media and the politicians. Where the BLS cannot measure meaningfully the impact of jobs loss and jobs creation from employers starting up or going out of business, on a timely basis (within at least five years, if ever), such information is estimated by the BLS along with the addition of a bias-factor generated by the BDM.

Positive assumptions—commonly built into government statistical reporting and modeling—tend to result in overstated official estimates of general economic growth. Along with happy guesstimates, there usually are underlying assumptions of perpetual economic growth in most models. Accordingly, the functioning and relevance of those models become impaired during periods of economic downturn, and the current downturn has been the most severe—in depth as well as duration—since the Great Depression.

Indeed, historically, the BDM biases have tended to overstate payroll employment levels—to understate employment declines—during recessions. There is a faulty underlying premise here that jobs created by start-up companies in this downturn have more than offset jobs lost by companies going out of business. So, if a company fails to report its payrolls because it has gone out of business (or has been devastated by a hurricane), the BLS assumes the firm still has its previously-reported employees and adjusts those numbers for the trend in the company’s industry.

Further, the presumed net additional “surplus” jobs created by start-up firms are added on to the payroll estimates each month as a special add-factor. These add-factors are set now to add an average of about 51,000 jobs per month in the current year. The aggregate overstatement of monthly jobs likely exceeds 100,000 jobs per month.

HOUSEHOLD SURVEY DETAILS. As discussed in the Concurrent Seasonal Factor Distortions, the seasonally-adjusted or headline September 2013 household-survey data are inconsistent with August 2013 and earlier reporting, due to the BLS’s unconscionable practice of revising previous estimates that are the basis for, and consistent with current reporting, but then publishing only the current number, not the consistent prior-period revisions. The BLS leaves in place earlier monthly estimates, knowing them to be inconsistent and not comparable with each other, let alone the current headline reporting. Accordingly, seasonally-adjusted month-to-month comparisons of components in the household survey are of no meaning.

Headline Household Employment. The household survey counts the number of people with jobs, as opposed to the payroll survey that counts the number of jobs (including multiple job holders more than once). On that basis, September 2013 employment rose by 133,000, after falling by 115,000 in August, but these numbers are not corrected for the unpublished and currently unknowable in-house BLS seasonal-adjustment revisions. Accordingly, as discussed in the Unemployment Rates section, the seasonally-adjusted household numbers in September are not legitimately comparable to the August.

Headline Unemployment Rates. Headline unemployment fell to 7.2% in September, from 7.3% in August. The September 2013 reading was down from an estimated 7.8% from the year before, but that annual decline generally is not good news, as discussed in Commentary No. 521 and Commentary No. 554. Instead of reflecting those who are unemployed finding jobs, the lower headline U.3 rate of recent months generally has reflected those who are unemployed being defined out of the government’s unemployment measurement by restrictive definitions.

Further, the reported September 2013 seasonally-adjusted headline (U.3) unemployment rate of 7.24% simply was not comparable to the 7.28% unemployment rate in August. Again, as with the other headline household-survey data, the problem with unemployment-rate comparability is tied to the use of concurrent-seasonal-factor adjustments.

When the seasonally-adjusted September 2013 unemployment data were calculated, consistent, new seasonal factors also were recalculated for August 2013 and prior months. Based on the new seasonal factors, there is a revised August unemployment rate that is consistent with September’s new headline reporting, but it is not available to the public. Although the BLS knows that number, it will not publish it; it has left intact the now-inconsistent and obsolete number that previously had been reported for August.

This pattern of inconsistent reporting is repeated every month, except in December when a revised and consistently seasonally-adjusted series is published. The misreporting process begins anew with the reporting of the unemployment data for each January (see the discussions in Commentary No. 451, Commentary No. 487 and the earlier Concurrent Seasonal Factor Distortions section for further detail).

As a result, the purported headline, 0.1% (0.04% to the second decimal place) month-to-month decline in the September U.3 employment rate could have been an increase, unchanged, or a decline, but no one other than the BLS knows for sure. Even so, the monthly decline in the official U.3 rate was statistically insignificant, based on official error estimates.

The official 95% confidence interval of +/- 0.23 percentage-point around the monthly headline U.3 number is meaningless in the context of comparative month-to-month reporting inconsistencies already discussed. On an unadjusted basis, however, the unemployment rates are not revised and are consistent in reporting methodology; they just are not adjusted for regular seasonal variations. September’s unadjusted U.3 unemployment rate was 7.0%, versus 7.3% in August.

U.6 Unemployment Rate. The broadest unemployment rate published by the BLS, U.6 includes accounting for those marginally attached to the labor force (including short-term discouraged workers) and those who are employed part-time for economic reasons (i.e., they cannot find a full-time job).

With minimal monthly changes for September in people working part-time for economic reasons and short-term discouraged workers, the headline September 2013 U.6-unemployment rate eased back to 13.6% from 13.7% in August, in tandem with the U.6 decline. Again, though, the monthly seasonally-adjusted numbers are not comparable, and the BLS guesstimates are unstable. The unadjusted September U.6 rate declined to 13.0%, from 13.6% in August. In a broader parallel with U.3, the decline in U.6 partially reflects long-term discouraged workers leaving the U.6 labor force and entering the realm of the ShadowStats alternate measure.

Discouraged Workers. The count of short-term discouraged workers (never seasonally-adjusted) was 852,000 in September, down from 866,000 in August 2013, versus 988,000 in July 2013, versus 1,027,000 in June, 780,000 in May, 835,000 in April, 803,000 in March, 885,000 in February and 804,000 in January. Those numbers still never will be comparable with the 1,068,000 of December 2012, thanks to the change in population assumptions that were published with the January 2013 data.

The current official discouraged-worker number reflected the flow of the unemployed—increasingly giving up looking for work—leaving the headline U.3 unemployment category and being rolled into the U.6 measure as short-term “discouraged workers,” net of those moving from short-term discouraged-worker status into the netherworld of long-term discouraged-worker status. It is the long-term discouraged-worker category that defines the ShadowStats-Alternate Unemployment Measure. There appears to have been a relatively heavy, continuing rollover from the short-term to the long-term category.

In 1994, “discouraged workers”—those who had given up looking for a job because there were no jobs to be had—were redefined so as to be counted only if they had been “discouraged” for less than a year. This time qualification defined away a large number of long-term discouraged workers. The remaining short-term discouraged workers (those discouraged less than a year) were included in U.6.

ShadowStats-Alternate Unemployment Rate. Adding back into the total unemployed and labor force the ShadowStats estimate of the growing ranks of excluded, long-term discouraged workers, broad unemployment—more in line with common experience, as estimated by the ShadowStats-Alternate Unemployment Measure—held again at 23.3% in September, as in August and July. July had notched lower from a series high of 23.4% (back to 1994) in June 2013. The ShadowStats estimate reflects the increasing toll of unemployed leaving the headline labor force. Where the ShadowStats alternate estimate generally is built on top of the official U.6 reporting, it tends to follow its relative monthly movements. Accordingly, the alternate measure often will suffer some of the same seasonal-adjustment woes that afflict the base series, including underlying annual revisions.

As seen in the usual graph of the various unemployment measures (in Opening Comments), there continues to be a noticeable divergence in the ShadowStats series versus U.6. The reason for this is that U.6, again, only includes discouraged workers who have been discouraged for less than a year. As the discouraged-worker status ages, those that go beyond one year fall off the government counting, even as new workers enter “discouraged” status.

With the continual rollover, the flow of headline workers continues into the short-term discouraged workers category (U.6), and from U.6 into long-term discouraged worker status (a ShadowStats measure). There was a lag in this happening as those having difficulty during the early months of the economic collapse, first moved into short-term discouraged status, and then, a year later into long–term discouraged status, hence the lack of earlier divergence between the series. The movement of the discouraged unemployed out of the headline labor force has been accelerating. See the Alternate Data tab for more detail.

Great Depression Comparisons. As discussed in previous writings, an unemployment rate above 23% might raise questions in terms of a comparison with the purported peak unemployment in the Great Depression (1933) of 25%. Hard estimates of the ShadowStats series are difficult to generate on a regular monthly basis before 1994, given the reporting inconsistencies created by the BLS when it revamped unemployment reporting at that time. Nonetheless, as best estimated, the current ShadowStats level likely is about as bad as the peak actual unemployment seen in the 1973 to 1975 and in the double-dip recession of the early-1980s.

The Great Depression unemployment rate of 25% was estimated well after the fact, with 27% of those employed working on farms. Today, less that 2% of the employed work on farms. Accordingly, a better measure for comparison with the ShadowStats number would be the Great Depression peak in the nonfarm unemployment rate in 1933 of roughly 34% to 35%.

CONSTRUCTION SPENDING (August 2013)

August Construction-Spending Increase Reflected Rising Costs. Total construction spending in August 2013 continued a monthly pattern of low-level stagnation, net of rising construction costs, with half of the nominal (not adjusted for inflation) August spending gain reflecting higher building costs, as opposed to increased volume of physical activity.

Although the general trend–even in nominal terms—has been minimally to the upside since 2011, monthly changes rarely have been statistically significant. The general pattern of activity has been one of plunge and stagnation, not the hyped GDP pattern of plunge and ever-after recovery, with recovery starting in mid-2009.

Official Reporting. The Census Bureau reported, today, October 22nd, that the total value of construction put in place in the United States during August 2013 was $915.1 billion, on a seasonally-adjusted—but not inflation-adjusted—annual-rate basis. That estimate was up month-to-month by a statistically-insignificant 0.6% +/- 2.5% (all confidence intervals are at a 95% level), versus a revised $909.4 (previously $900.8) billion in July. Before prior-period revisions, July reporting would have reflected a monthly gain of 1.6%.

Adjusted for PPI new construction inflation, aggregate real spending in August 2013 was up by 0.3% month-to-month, versus a 1.4% gain in July.

On an annual-growth basis, August 2013 construction spending was up year-to-year by a statistically-significant 7.1% +/- 2.7%, versus a revised July annual gain of 6.2%. Net of construction costs indicated by the PPI current construction index, year-to-year growth in spending was 5.7% in August, 4.1% in July 2013. More-realistic private surveying suggests annual costs to be up by enough to come close to turning those annual construction-spending growth rates flat or into annual contractions.

The statistically-insignificant 0.6% gain in monthly August 2013 construction spending included a 0.4% monthly gain in public construction spending, versus a revised 0.1% month-to-month gain (previously a 0.3% contraction) in July. August private construction was up by 0.7%, following a revised 1.9% (previously 0.9%) gain in July. The accompanying graphs, including the first graph following, show the 0.6% monthly gain in August total construction, with private residential construction up by 1.2%, private nonresidential construction up by 0.1% and public construction up by 0.4% for the month.

The preceding two graphs reflect total construction spending through August 2013, the first is before inflation adjustment; the second is an aggregate index reflecting inflation-adjusted data. The second graph (see also Opening Comments) shows the August 2013 ShadowStats estimation of an inflation-adjusted construction spending series. Suggestive of the August monthly gain largely reflecting higher costs, instead of increased physical construction volume.

There is no perfect inflation measure for deflating construction, but the PPI new construction index is the closest found in publicly available series. Adjusted for the PPI measure, construction spending shows the economy slowing in 2006, plunging into 2011 and then turning minimally higher in an environment of low-level stagnation, through the most-recent reporting. The pattern of inflation-adjusted activity here does not confirm the economic recovery shown in the headline GDP series (see Commentary No. 561). To the contrary, the latest construction reporting, both before and after inflation adjustment, shows a pattern of ongoing stagnation.

The next graph reflects the reporting of September 2013 construction employment, released this morning, with headline, seasonally-adjusted construction employment up by 20,000 in the month, at 5.826 million.

The next two graphs cover private residential construction, including housing starts data, as last reported for August 2013 (see Commentary No. 558 for detail). The difference in the graphs is the smoother pace of actual spending (not-adjusted-for-inflation), instead of the more-irregular monthly variation in the count of physical monthly starts.

The last two graphs preceding show the patterns of the monthly level of activity in private nonresidential construction spending and in public construction spending. The spending in public construction spending, which is 98% nonresidential, has been in a broad downtrend following a short-lived upside bounce in 2010.

EXISTING-HOME SALES (September 2013)

Slowing of Annual Growth Continued; September Monthly Decline Muted by Downside August Revision. Despite the positive hype surrounding existing home sales, the 1.9% decline in September monthly home sales would have been 3.5% without the downside revision to August sales. Year-to-year growth continued to slow, dropping to 10.7% in September, from 11.4% (previously 13.2%) in August, from its near-term peak of 17.2% in July, while the latest activity remained 27.2% below the June 2005 pre-recession high for the series.

Given questions of the series’ reliability, particularly the quality of, and the volatility, instabilities and uncertainties in the reporting of existing-home sales, not too much should be read into the reported trends. These data will be reviewed in the context of the next publication of new home sales and residential construction.

September 2013 Existing-Home Sales Reporting. Yesterday’s (October 21st) release of September 2013 existing-home sales (counted based on actual closings, National Association of Realtors [NAR]) showed a seasonally-adjusted monthly contraction of 1.9%, versus a revised “unchanged” reading in August (previously a 1.7% monthly gain). Net of the prior-period revision, the September month-to-month contraction would have been 3.5%.

The September decline to a seasonally-adjusted, monthly-unit sales pace of 440,800 (5,290,000 annualized) from a revised 449,200 (5,390,000 annualized), which previously was 456,700 (an annualized pace of 5,480,000), still was within normal month-to-month volatility for this otherwise highly unstable series. On a year-to-year basis, September 2013 annual sales slowed to 10.7%, from a revised 11.4% (previously 13.2%) in August.

Smoothed for irregular distortions, the series remained statistically consistent with a period of broad stagnation that has turned into a faltering uptrend, as suggested by the graph shown in the Opening Comments. Again, the data remain of questionable enough quality to leave the indicated trend highly uncertain.

The portion of total sales in distressed properties rose in the latest reporting, from August’s post-2008 Crisis low. The NAR estimated “distressed” sales in September 2013 jumped to 14% of the total (9% foreclosures, 5% short sales), versus 12% of the total (8% foreclosures, 4% short sales) in August.

Reflecting ongoing lending problems, related banking-industry and consumer solvency issues, and the continuing influx of speculative investment money into the existing housing market, the NAR also estimated that all-cash sales in September 2013 were at 33% of the total, up from 32% in August 2013 and 28% in September 2012.

As discussed most recently in Commentary No. 564, there have been no developments in underlying economic fundamentals that would suggest a pending housing-industry turnaround or broad economic recovery.

__________

WEEK AHEAD

Weaker-Economic and Stronger-Inflation Reporting Likely in the Months Ahead. See the schedule for the latest detail, including the rescheduling of the delayed September and October economic reporting in the post-government shutdown period. [Other than for the completely new detail of next week’s pending releases, this Week Ahead section is unchanged from Commentary No. 564 of October 11th.]

Despite continuing downside adjustments to consensus expectations on the domestic economy, the markets still are overly optimistic. That circumstance, and underlying fundamentals that are suggestive of deteriorating business activity, mean that weaker-than-consensus economic reporting should remain the general trend. Inflation likely will be higher than market expectations.

In terms of monthly inflation reporting, energy-inflation-related seasonal-adjustment factors are on the plus-side through the end of the year. That, combined with likely stable or higher oil and gasoline prices, means stronger-than-expected headline CPI and PPI are a good bet for at least the next four months, and beyond. Upside pressure on oil-related prices should reflect intensifying impact from a weakening U.S. dollar in the currency markets, and from ongoing political instabilities in the Middle East. The dollar faces pummeling from continuing QE3, and the soon-to-resurface fiscal-crisis/debt-ceiling debacle (see opening comments and the Hyperinflation Outlook section). Particularly in tandem with the likely weakened dollar, inflation reporting in the year ahead generally should reflect much higher-than-expected inflation (see also No. 527: Special Commentary).

A Note on Reporting Quality Issues and Systemic Reporting Biases. Significant reporting-quality problems remain with most major economic series. Headline reporting issues are tied largely to systemic distortions of seasonal adjustments. The data instabilities were induced by the still-ongoing economic turmoil of the last six-to-seven years, which has been without precedent in the post-World War II era of modern economic reporting. These impaired reporting methodologies provide particularly unstable headline economic results, where concurrent seasonal adjustments are used (as with retail sales, durable goods orders, employment and unemployment data), and they have thrown into question the statistical-significance of the headline month-to-month reporting for many popular economic series.

PENDING RELEASES:

U.S. Trade Balance (August 2013). The August trade deficit has been rescheduled for release on Thursday, October 24th, by the Census Bureau and the Bureau of Economic Analysis (BEA). While the markets appear to be expecting little change in the monthly deficit, heavy reporting distortions from trade-flow disruptions could have major impact (see Commentary No. 548). Underlying trade-related fundamentals and long-term trends continue to favor significant and ongoing trade-deficit deterioration.

Any significant swing in the data would impact the upcoming initial estimate of third-quarter GDP, now scheduled for November 7th. A wider-than-expected deficit in the trade numbers would have negative implications for the expectations of headline GDP growth.

New Orders for Durable Goods (September 2013). The Census Bureau has scheduled release of September 2013 new orders for durable goods for Friday, October 25th. Other than for the continuing sharp and irregular volatility in commercial aircraft orders, new orders generally have been stagnant. Once again, some intensification of recent, sporadic downside movement in orders remains likely during the next several months, coincident with slowing activity evident in other economic indicators. Such reporting generally would tend to surprise market expectations on the downside, beyond any expected increase in commercial aircraft orders.

As to the inflation contribution to the monthly and annual change in new orders, that awaits the rescheduled September 2013 PPI finished goods capital equipment inflation index on October 29th, as discussed below.

Index of Industrial Production (September 2013). The September 2013 index of industrial production was rescheduled for Monday, October 28th, by the Federal Reserve Board. Inventories still are too high for existing demand, and an outright monthly contraction in production remains a fair bet. Minimally, continuing downside surprises to artificially high expectations are likely in September production, as are continuing downside revisions to prior-period reporting. The federal government shutdown should have some negative impact on the production in the month of October, which will be released in November.

Retail Sales (September 2013). The September 2013 retail sales estimate was rescheduled for release on Tuesday, October 29th, by the Census Bureau. With the structural liquidity issues increasingly constraining consumer activity, once again, odds favor the headline retail sales reporting to come in below market expectations. An outright month-to-month sales contraction is a good possibility, even before adjustment for consumer inflation.

Producer Price Index—PPI (September 2013). The September 2013 PPI was rescheduled for release on Tuesday, October 29th, by the Bureau of Labor Statistics (BLS). For September, PPI energy prices face relatively positive seasonal factor biases. Given still-understated food inflation and ongoing upside “core” inflation, the headline PPI should come in on the plus-side.

Depending on the oil contract followed, oil prices, on average, were up or down by 0.3% for the month of September, with average retail gasoline prices down by 1.1% for the second month. Accordingly, with positive seasonal adjustments to energy prices, a small monthly gain in PPI again is a good bet.

Consumer Price Index—CPI (September 2013). The release by the Bureau of Labor Statistics (BLS) of the August 2013 CPI numbers has been rescheduled for Wednesday, October 30th. The headline CPI is a fair bet to come in around the market consensus of about 0.1% to 0.2%.

Average gasoline prices eased month-to-month in September 2013 by 1.1 percentage point, on a not-seasonally-adjusted basis, per the Department of Energy. The BLS seasonal adjustments, however, should offset the nominal monthly decline in gasoline prices. As last revised, an unadjusted monthly 2.2% gain in September 2012 gasoline prices was widened to a 4.1% gain, with upside seasonal adjustments. Similar effects in the September 2013 number would push the unadjusted monthly gasoline price contraction to the plus-side, contributing roughly 0.1 percentage point to the aggregate headline CPI-U number. Given likely upside inflation pressures from food prices and core inflation, a small headline gain in September 2013 CPI-U is a reasonable expectation.

Year-to-year, CPI-U inflation would increase or decrease in September 2013 reporting, dependent on the seasonally-adjusted monthly change, versus an adjusted 0.52% increase in monthly inflation reported for September 2012. The adjusted change is used here, since that is how consensus expectations are expressed. To approximate the annual unadjusted inflation rate for September 2013, the difference in September’s headline monthly change (or forecast of same), versus the year-ago monthly change, should be added to or subtracted directly from the August 2013 annual inflation rate of 1.52%.

For example, if the headline September CPI-U inflation were 0.1%, annual inflation would slow to approximately 1.1%.

__________